Master Resale Rights (MRR) for busy entrepreneurs: Learn how to sell done-for-you digital products, create passive income, and build an online business without starting from scratch.

:max_bytes(150000):strip_icc()/financial-independence-retire-early-fire-c928050718c9429584e88a5df23ebb1d.jpg)

Updated: July 15, 2025

20 min read

45 Comments

Introduction

Welcome to the ultimate guide on achieving financial independence and retiring early. In this comprehensive article, we will delve into the key concepts, strategies, and considerations for attaining financial freedom and enjoying an early retirement. Whether you're a seasoned investor or just beginning your financial journey, this guide will provide valuable insights to help you pave the path towards financial independence.

The FIRE (Financial Independence, Retire Early) movement has gained significant traction in recent years, as more people seek to break free from the traditional 9-5 grind and live life on their own terms. This guide will walk you through each step of the FIRE journey, from understanding the core concepts to implementing practical strategies that can help you achieve your financial independence goals.

What is Financial Independence and Early Retirement?

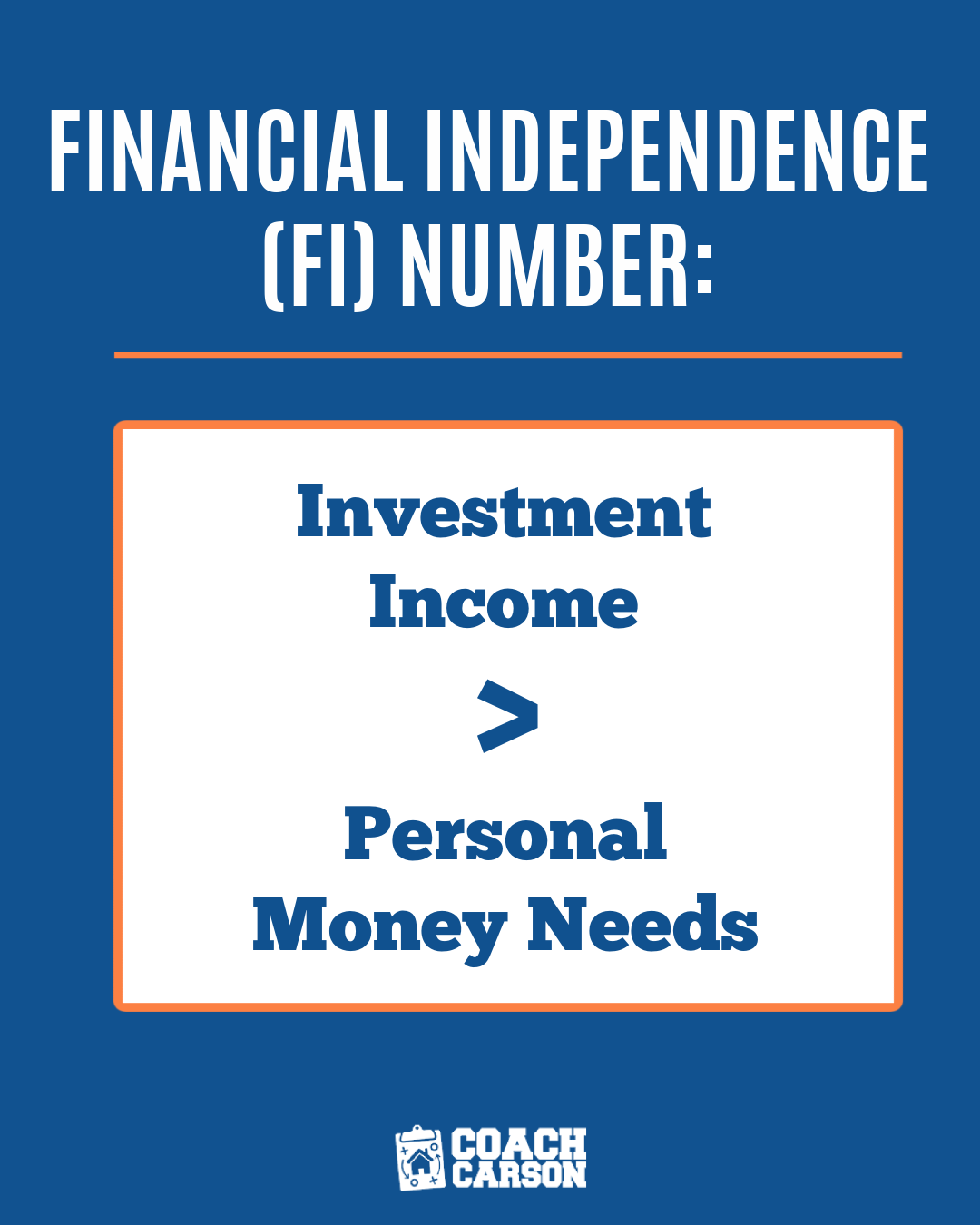

Financial independence is the state of having sufficient wealth to sustain your desired lifestyle without the need for active employment. This means that you have enough passive income to cover your expenses and can choose how you spend your time, whether it's pursuing your passions, spending time with loved ones, or engaging in meaningful activities.

Early retirement, on the other hand, involves exiting the workforce and ceasing full-time employment at an age younger than the traditional retirement age. This can be achieved through a combination of financial independence and careful planning.

FIRE Types

-

Traditional FIRE

Standard approach aiming for 25x annual expenses

-

Fat FIRE

Retirement with above-average spending

-

Lean FIRE

Minimalist lifestyle with lower expenses

-

Barista FIRE

Part-time work covering basic expenses

Financial independence isn't about being rich. It's about having the freedom to make life decisions without being overly stressed about the financial impact.

The FIRE movement is built on several core principles, including extreme savings rates, frugal living, and strategic investing. Followers of the FIRE movement typically aim to save between 50% and 75% of their income, far exceeding the conventional financial advice of saving 10-15% of your income for retirement.

Why Achieving Financial Independence and Retiring Early Matters

Attaining financial independence and retiring early holds significant importance in today's dynamic world. It empowers individuals to break free from the constraints of a paycheck-to-paycheck existence, mitigates the impacts of financial stress, and opens doors to a realm of possibilities.

Freedom and Flexibility

By achieving financial independence and retiring early, individuals have the freedom to choose how they want to spend their time. They can pursue their passions, travel, or simply relax without the constraints of a 9-5 job.

Reduced Stress

Financial stress is a major concern for many individuals. By achieving financial independence and retiring early, individuals can eliminate this stress and focus on their well-being and personal growth.

Personal Growth

Early retirement provides individuals with the time and resources to invest in personal growth. This can include learning new skills, pursuing hobbies, or even starting a new business.

Quality Time

FIRE allows you to spend more time with family and friends, creating deeper relationships and meaningful experiences that might otherwise be limited by work schedules.

Beyond these immediate benefits, financial independence creates security and resilience against economic downturns, job losses, or health issues. It provides a safety net that allows you to face life's challenges with confidence, knowing that your basic needs are covered regardless of external circumstances.

How to Calculate Your Financial Independence Number

Calculating your financial independence number is a pivotal step in embarking on the journey towards financial freedom and early retirement. This figure represents the amount of wealth required to sustain your desired lifestyle without the need for ongoing employment income.

The Basic FIRE Formula

Financial Independence Number = Annual Expenses × 25

Based on the 4% Safe Withdrawal Rate

Step-by-Step Calculation:

1

Calculate your annual expenses

Add up all your essential and discretionary expenses for a year. Be comprehensive and realistic about your spending habits.

2

Adjust for retirement lifestyle changes

Consider how your expenses might change in retirement. You might spend less on commuting but more on hobbies or travel.

3

Multiply by 25 (for a 4% withdrawal rate)

This is based on the "4% Rule," which suggests that you can safely withdraw 4% of your portfolio in the first year of retirement, and then adjust that amount for inflation in subsequent years.

4

Account for additional income sources

If you'll have other income sources in retirement (Social Security, pension, part-time work), you can reduce your FIRE number accordingly.

Example Calculation:

- Annual Expenses: $60,000

- Multiplication Factor (25): Based on 4% withdrawal rate

- FIRE Number: $60,000 × 25 = $1,500,000

- With Additional Annual Income (e.g., $10,000): ($60,000 - $10,000) × 25 = $1,250,000

It's important to regularly reassess your FIRE number as your life circumstances, expenses, and retirement goals may change over time. Consider building in a buffer for unexpected expenses or market downturns to make your plan more resilient.

Strategies for Achieving Financial Independence and Retiring Early

Embarking on the quest for financial independence and early retirement necessitates the implementation of shrewd strategies and prudent financial decisions. From astute investment approaches to disciplined budgeting, an array of proven tactics can expedite the realization of these lofty goals.

Increase Your Savings Rate

The most powerful lever in achieving FIRE is your savings rate—the percentage of your income that you save and invest. The higher your savings rate, the faster you'll reach financial independence.

"The math behind early retirement is shockingly simple. The higher your savings rate, the sooner you'll reach financial independence." — Mr. Money Mustache

Reduce Expenses

Cutting unnecessary expenses has a double benefit: it increases your savings rate now and reduces the amount you'll need in retirement. Focus on big-ticket items like housing, transportation, and food.

Maximize Income

While cutting expenses is important, increasing your income can accelerate your journey to FIRE. Consider negotiating a raise, switching to a higher-paying job, developing new skills, or starting a side hustle.

Smart Investing

Invest early and consistently. Take advantage of tax-advantaged accounts, keep investment costs low, and create a diversified portfolio aligned with your risk tolerance and time horizon.

Build Multiple Income Streams

Diversifying your income sources provides financial stability and can accelerate wealth building. Consider developing passive income streams through investments, real estate, or business ventures.

The path to FIRE is not a one-size-fits-all approach. You'll need to tailor these strategies to your own circumstances, preferences, and goals. The key is to maintain consistency and persistence, making regular adjustments as needed to stay on track.

Maximizing Savings and Investments for Early Retirement

Optimizing savings and investments is a pivotal component in the pursuit of early retirement. By prioritizing a robust savings plan, individuals can accumulate a substantial financial reservoir that lays the groundwork for a secure and comfortable post-employment lifestyle.

Investment Vehicles for FIRE

Tax-Advantaged Accounts

Maximize contributions to 401(k)s, IRAs, and HSAs to reduce taxes and accelerate growth.

Index Funds

Low-cost index funds provide diversification and historically reliable returns with minimal fees.

Real Estate

Rental properties or REITs can provide passive income and potential appreciation.

Dividend Stocks

Companies that pay regular dividends can provide growing passive income over time.

Investment Principles for FIRE

- Start early to maximize compound growth

- Automate investments to maintain consistency

- Keep costs low through index funds and ETFs

- Maintain proper asset allocation based on your time horizon

- Rebalance periodically to maintain your target allocation

- Stay the course during market volatility

- Continually educate yourself about investing

The Power of Compound Interest

Compound interest is the eighth wonder of the world, allowing your money to grow exponentially over time. The earlier you start investing, the more time your money has to compound and grow.

Advanced Investment Strategies for FIRE

Tax-Efficient Fund Placement

Place tax-inefficient investments (like bonds and REITs) in tax-advantaged accounts, and tax-efficient investments (like index funds) in taxable accounts to minimize your tax burden.

Roth Conversion Ladder

This strategy allows early retirees to access retirement funds before age 59½ without penalties by systematically converting traditional IRA funds to a Roth IRA and waiting five years before withdrawal.

Tax-Loss Harvesting

Strategically sell investments at a loss to offset capital gains taxes while maintaining your overall investment strategy through similar but not identical investments.

Maximizing your savings and investments requires discipline, knowledge, and strategic planning. By implementing these strategies, you can accelerate your journey to financial independence and set yourself up for a successful early retirement.

Managing Expenses to Achieve Financial Independence

Effectively managing expenses is a critical facet in the endeavor to achieve financial independence. By adopting prudent spending habits, cultivating fiscal discipline, and differentiating between needs and wants, individuals can streamline their financial outlays and bolster their capacity to accumulate wealth.

The Expense Reduction Hierarchy

Focus your efforts on reducing expenses in order of impact:

1

Housing

Typically your largest expense. Consider downsizing, house hacking, or relocating to a lower-cost area.

2

Transportation

Reduce or eliminate car payments, consider public transport, biking, or walking when possible.

3

Food

Cook at home, meal plan, buy in bulk, and reduce dining out to significantly cut food costs.

4

Recurring Bills

Audit subscriptions, negotiate bills, and eliminate services you don't fully utilize.

Practical Expense Management Strategies

Create a Detailed Budget

Track every expense to understand where your money goes. Use apps like Mint, YNAB, or Personal Capital to automate this process and categorize spending.

Eliminate High-Interest Debt

Prioritize paying off credit cards and other high-interest debt. This provides an immediate return equal to the interest rate you're paying.

Practice Mindful Spending

Before making purchases, especially large ones, implement a waiting period (e.g., 30 days) to ensure it's a need rather than an impulse.

Avoid Lifestyle Inflation

As your income increases, resist the urge to increase spending proportionally. Instead, direct raises and bonuses toward savings and investments.

The Latte Factor: Small Expenses Add Up

While big expenses like housing have the largest impact, don't overlook the cumulative effect of small daily expenses.

| Expense | Daily Cost | Monthly Cost | Annual Cost | 10-Year Investment* |

|---|---|---|---|---|

| Coffee Shop Coffee | $5 | $150 | $1,825 | $25,800 |

| Lunch Out | $12 | $240 | $2,880 | $40,700 |

| Subscription Services | $1.50 | $45 | $540 | $7,640 |

*Assuming 7% annual return

Managing expenses doesn't mean eliminating all enjoyment from your life. It's about being intentional with your spending, focusing your resources on what truly brings value, and eliminating waste. By reducing expenses, you not only increase your savings rate but also permanently reduce the amount you'll need to reach financial independence.

Building Multiple Streams of Income

Diversifying income streams is an instrumental strategy in the pursuit of financial independence and early retirement. By generating multiple sources of revenue, individuals can buttress their financial foundation, enhance their savings potential, and fortify their long-term financial security.

Types of Income Streams

Active Income

Requires your direct time and effort (e.g., salary, wages, consulting)

Passive Income

Requires minimal ongoing effort after initial setup (e.g., investments, royalties)

Portfolio Income

Generated from investments (e.g., dividends, capital gains, interest)

Passive Income Opportunities

Real Estate Investments

- • Rental properties (residential or commercial)

- • Real Estate Investment Trusts (REITs)

- • Real estate crowdfunding platforms

- • House hacking (renting out portions of your home)

Dividend Investing

- • Dividend-paying stocks

- • Dividend ETFs and mutual funds

- • Dividend aristocrats (companies with consistent dividend increases)

- • Dividend reinvestment plans (DRIPs)

Digital Products

- • E-books and online courses

- • Software, apps, or website templates

- • Stock photography, music, or digital art

- • Membership sites or subscription services

Affiliate Marketing

- • Product reviews and recommendations

- • Niche websites focused on specific topics

- • Email marketing to promote affiliate products

- • YouTube channels with affiliate links

E-commerce

- • Dropshipping stores

- • Print-on-demand merchandise

- • Amazon FBA (Fulfillment by Amazon)

- • Automated e-commerce systems

Peer-to-Peer Lending

- • Lending platforms like Prosper or Lending Club

- • Real estate crowdlending

- • Business lending opportunities

- • Microloans to entrepreneurs

Income Stream Development Strategy

- 1. Start with your expertise: Begin building income streams in areas where you already have knowledge or skills.

- 2. Focus on one stream at a time: Master one income source before moving on to the next to avoid spreading yourself too thin.

- 3. Diversify across categories: Balance active and passive income, as well as different asset classes and industries.

- 4. Reinvest profits: Use earnings from established income streams to fund and grow new ones.

- 5. Automate where possible: Implement systems and processes to minimize the ongoing time requirement for each income stream.

Building multiple streams of income takes time and effort, but the long-term benefits for your financial independence journey are substantial. As you develop diverse income sources, you'll create resilience against economic downturns, accelerate your savings rate, and ultimately build a more secure path to early retirement.

Benefits of Achieving Financial Independence and Retiring Early

Realizing financial independence and retiring early bestows a myriad of transformative benefits that transcend mere financial considerations. Beyond the realm of monetary prosperity, early retirement affords individuals the liberty to pursue personal passions, invest in lifelong pursuits, and devote ample time to familial and altruistic endeavors.

Embracing financial independence cultivates a sense of empowerment, enabling individuals to lead purposeful, enriching lives unconstrained by financial obligations or the exigencies of a conventional career.

Time Freedom

The most precious resource is time. FIRE gives you back your time to use as you choose, without the constraints of a mandatory work schedule.

Mental Wellbeing

Reducing financial stress and eliminating workplace pressures can significantly improve mental health and overall quality of life.

Relationship Quality

More time for family and friends means deeper, more meaningful relationships and the ability to be present for important moments.

Pursue Passions

Follow interests and hobbies without concern for their income potential—do what you love simply because you love it.

Travel Flexibility

Travel during off-peak times, stay longer in destinations, and experience places more deeply without vacation time constraints.

Giving Back

Volunteer, mentor, or contribute to causes you care about with your most valuable asset—your time and attention.

"Financial independence isn't about being rich. It's about having options. It's about being able to say 'no' to things you don't want to do and 'yes' to things that matter."

Long-Term Benefits of FIRE

- Financial resilience during economic downturns or personal emergencies

- Improved physical health through reduced stress and more time for exercise

- Opportunity for personal growth and continuous learning

- Community involvement and deeper social connections

- Environmental benefits from potentially reduced consumption

- Legacy building through knowledge sharing and mentorship

The benefits of financial independence and early retirement extend far beyond financial security. They touch every aspect of your life, from health and relationships to personal fulfillment and community impact. While the journey to FIRE requires discipline and sacrifice, the freedom and opportunities it provides make it a worthy pursuit for those seeking a more intentional and self-directed life.

Retirement Plans and Withdrawal Strategies

Developing robust retirement plans and astute withdrawal strategies is pivotal in ensuring a seamless transition into early retirement. By meticulously crafting retirement plans tailored to individual circumstances, aligning them with risk tolerance, and optimizing withdrawal strategies, individuals can safeguard their post-employment financial security.

The 4% Rule Explained

The 4% rule is a cornerstone of retirement planning in the FIRE community. Developed by financial advisor William Bengen and later validated by the Trinity Study, this rule suggests that retirees can withdraw 4% of their initial portfolio value in the first year of retirement, then adjust that amount for inflation each subsequent year.

Based on historical market performance, this withdrawal rate has a high probability of sustaining a portfolio for at least 30 years, making it particularly relevant for traditional retirement planning. For early retirees who may need their money to last 40-50 years or more, some financial experts recommend a more conservative withdrawal rate of 3-3.5%.

Alternative Withdrawal Strategies

Variable Percentage Withdrawal (VPW)

Instead of withdrawing a fixed percentage adjusted for inflation, this method recalculates the withdrawal percentage each year based on remaining portfolio balance and life expectancy. This approach adapts to market conditions but may result in fluctuating annual income.

Guardrails Strategy

This approach establishes upper and lower bounds for withdrawal rates. If portfolio performance pushes the withdrawal rate outside these guardrails, you adjust spending accordingly. This provides flexibility while preventing excessive withdrawals during market downturns.

Bucket Strategy

Divide your portfolio into different "buckets" based on when you'll need the money. Near-term expenses go in conservative investments (cash, bonds), while long-term needs stay in growth investments. This helps manage sequence of returns risk.

Yield Shield

Focus on generating income through dividends, interest, and other yields rather than selling assets. This can provide more stability during market downturns but may require a larger portfolio or acceptance of lower total returns.

Tax-Efficient Withdrawal Strategies

Minimizing taxes is a critical component of an effective withdrawal strategy. Here are some approaches to consider:

Tax Bracket Management

Strategically withdraw from different account types (taxable, tax-deferred, tax-free) to optimize your tax situation each year. Stay within lower tax brackets when possible.

Roth Conversion Ladder

Systematically convert traditional IRA/401(k) funds to Roth accounts during low-income years. After a five-year waiting period, you can access these conversions penalty-free, even before age 59½.

Capital Gains Harvesting

Strategically realize capital gains in years when your income is low enough to qualify for the 0% long-term capital gains tax rate (up to certain income thresholds).

Rule 72(t) Distributions

Take substantially equal periodic payments (SEPPs) from retirement accounts before age 59½ without the usual 10% early withdrawal penalty, following specific IRS guidelines.

Factors to Consider When Developing Your Withdrawal Strategy

Time Horizon

Early retirees need their money to last significantly longer than traditional retirees, which may necessitate a more conservative approach.

Market Conditions

Sequence of returns risk (experiencing poor returns early in retirement) can significantly impact portfolio longevity. Have contingency plans for market downturns.

Health and Longevity

Consider your health status and family history when planning for longevity. Medical expenses often increase with age.

Tax Environment

Tax laws change over time. Build flexibility into your plan to adapt to evolving tax regulations.

Flexibility in Expenses

The ability to adjust spending during market downturns can significantly improve portfolio sustainability.

Housing Strategy

Consider whether downsizing, relocating, or tapping home equity through a reverse mortgage might play a role in your retirement plan.

Your withdrawal strategy should be personalized to your specific circumstances and retirement goals. It's often beneficial to work with a financial advisor who understands the unique challenges of early retirement to develop a robust plan. Remember that any strategy should be reviewed and potentially adjusted regularly as your situation and market conditions evolve.

Frequently Asked Questions

What is the FIRE movement?

FIRE stands for Financial Independence, Retire Early. It's a movement focused on extreme savings and investment strategies that allow people to retire much earlier than traditional retirement age. The core principle is to save and invest a high percentage of your income (typically 50-70%) to build a portfolio that can sustain your living expenses through investment returns.

How much money do I need to achieve financial independence?

The commonly accepted guideline is to accumulate 25 times your annual expenses, based on the 4% safe withdrawal rate. For example, if you spend $40,000 per year, you'd need approximately $1 million invested to be financially independent. However, this number can vary based on your desired lifestyle, location, healthcare needs, and other factors. Some early retirees who want more security aim for 28-33 times their annual expenses.

How long does it take to achieve FIRE?

The time required to achieve FIRE depends primarily on your savings rate (the percentage of your income you save and invest) and investment returns. At a 50% savings rate with average market returns, it typically takes about 15-17 years to reach financial independence. At a 70% savings rate, this can drop to around 10 years. Your income level, investment strategy, and market performance will all impact this timeline.

Is the 4% withdrawal rule still valid?

The 4% rule remains a helpful guideline, but some financial experts suggest it may be too aggressive for early retirees with extremely long retirement horizons (40+ years) or during periods of high market valuations and low interest rates. For those seeking more security, a 3-3.5% withdrawal rate might be more appropriate. The key is to remain flexible with your withdrawals and adjust based on market conditions and your personal circumstances.

How do I access retirement funds before age 59½ without penalties?

Several strategies can help you access retirement funds early without incurring the usual 10% penalty:

- Roth IRA conversion ladder (convert traditional funds to Roth, then withdraw contributions after 5 years)

- Rule 72(t) distributions (Substantially Equal Periodic Payments)

- Utilizing taxable accounts first

- Withdrawing Roth IRA contributions (not earnings) penalty-free

- Using specific exceptions to the early withdrawal penalty (first-time home purchase, qualified education expenses, etc.)

What about healthcare before Medicare eligibility?

Healthcare is often one of the biggest concerns for early retirees. Options include:

- Health insurance through the ACA marketplace (potentially with subsidies depending on your taxable income)

- Health sharing ministries (though these are not traditional insurance)

- Part-time work that offers health benefits

- Coverage through a working spouse

- Medical tourism for certain procedures

- Building a larger investment cushion specifically for healthcare expenses

What are the different types of FIRE?

The FIRE movement has evolved to include several variations:

- Traditional FIRE: Accumulating 25x annual expenses (typically $1-2 million)

- Fat FIRE: Retiring with a higher annual budget for a more luxurious lifestyle (often $100,000+ annually)

- Lean FIRE: Minimalist approach with significantly reduced expenses (often under $40,000 annually)

- Barista FIRE: Semi-retirement with part-time work covering basic expenses while investments grow

- Coast FIRE: Having enough invested that, without additional contributions, your portfolio will grow to support retirement at a traditional age

Conclusion

As we conclude this comprehensive guide on achieving financial independence and retiring early, it's imperative to underscore the transformative potential of these pursuits. Financial independence and early retirement not only engender unparalleled financial security but also lay the foundation for a life of purpose, fulfillment, and personal empowerment.

The journey to FIRE is as individual as you are. There's no one-size-fits-all approach, and your path will be shaped by your unique circumstances, values, and goals. Whether you're drawn to the minimalist lifestyle of Lean FIRE or aspire to the more abundant Fat FIRE, the core principles remain the same: increase your savings rate, invest wisely, manage expenses intentionally, and build multiple income streams.

Remember that financial independence is not just about the destination—it's about the journey. Along the way, you'll develop valuable skills, habits, and mindsets that will serve you well regardless of when or whether you ultimately retire. The financial discipline, intentionality, and clarity of purpose that come with pursuing FIRE can enhance your life immediately, even as you work toward your longer-term goals.

Key Takeaways

Calculate your FIRE number (typically 25x your annual expenses) to establish a clear target

Maximize your savings rate (aim for 50%+ of income) to accelerate your journey

Invest consistently and wisely, focusing on low-cost index funds for long-term growth

Manage expenses intentionally, cutting costs that don't align with your values

Build multiple income streams to accelerate wealth accumulation and create resilience

Develop a sustainable withdrawal strategy aligned with your time horizon and risk tolerance

Remain flexible and adapt your plan as circumstances and market conditions change

By meticulously crafting actionable plans, embracing astute investment strategies, and nurturing disciplined financial habits, you can chart a course toward financial freedom and early retirement, transcending the boundaries of traditional employment and embracing a life of autonomy, abundance, and fulfillment. The path may not always be easy, but the freedom waiting at the end is worth every careful step along the way.